Living in the house you own is the script society tells you. But it often doesn’t make sense. Still, people seem to think they totally made it when they finally buy their first house. Home ownership makes a lot of sense, but living in it yourself doesn’t.

Buying a house is probably the biggest financial transaction in your life. Buying a house to live in, usually with your partner, brings lots of emotions. Emotions are the worst thing to have when making financial decisions.

If you want to buy a house, treat it as an investment decision, not an emotional one.

Own a house to rent out as investment

Rent a house to live in it https://t.co/kQymBcLbwv

— @levelsio (@levelsio) June 7, 2019

I just read Robert Kiyosaki’s classic book Rich Dad Poor Dad, that confirmed my beliefs on this topic.

Kiyosaki had two dads. His real father (poor dad), a highly educated man with a good job, told him to study in order to get a well paying job to be able to buy a house, his stepfather (rich dad), an entrepreneur and investor without education, told him to get financially literate in order to look for assets that make money work for him.

He decided to follow his rich dad.

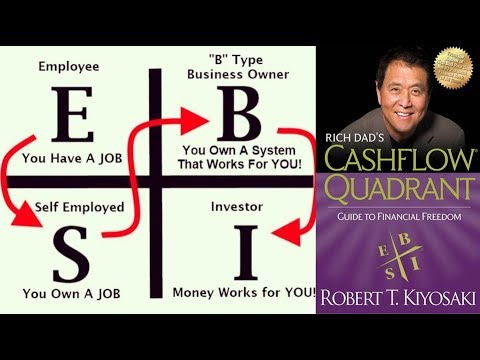

This author also developed the cashflow quadrant. On the left side of this quadrant are the employees (people that have a job) and the freelancers (people that are a job), on the right side are the entrepreneurs (people that own a system) and the investors (people that make money with money).

People on the left side work for money while people on the right side let money work for them. You should get to the right side as early in your life as possible if you want to reach financial independence on a certain moment. Don’t forget to watch the video.

Our society has encouraged us to learn a profession so we can work for money, but failed to teach us how to have money work for us. The vast majority of the Western world subscribes to this dogma, simply because it’s easier to find a job and work for money than to take risks and get rich. These are the same people that tell you to not rent a house.

A house you live in is not an asset but a liability, because it doesn’t make you money. Something that you have to pay instead that it pays you, is not a good investment. Rich people acquire assets while the poor acquire liabilities that they think are assets.

A house you rent is an asset when it makes you more money every month than the mortgage you pay to the bank. A mortgage is a way to leverage your investment and its returns, and helps you to start becoming an investor early in life, which makes a gigantic difference due to the compound effect.

In most countries you have to bring a minimum percentage of own money to the table to get a mortgage for investment property. Based on the savings you have, you can calculate what your first investment can be. This can be as small as a storage box to start with, as long as you can rent it out with profit.

After that, you can refinance your first property and use it as collateral for your next one, and build a portfolio like that. The first property of a portfolio is the most important and the hardest one, that’s why it’s crucial to start early.

But you have to live somewhere, right? It’s highly improbable that this will be the same place for thirty years, the length of a standard mortgage. If you leave earlier it’s uncertain if your property’s value has increased, which usually is a long term effect.

If the value has increased, it’s probably because of inflation, and the price of your new house has also increased, eating your profit. And you have to pay all the additional costs again, like notary, taxes and renovations.

If you are renting your home while building your portfolio, in the beginning you break even or even make loss, while buying a home would lower your monthly expenses at that moment.

I understand it seems obvious to go for the latter in that phase, as it’s hard to think long term. But the compound effect applies greatly here.

It’s an urban myth that renting is throwing away money, propagated by real estate agents and banks to make you buy. Beware that houses were built for banks, not for people.

Renting gives you freedom, which is my most important life value. You might change jobs, cities, relationships or have children. Renting allows you to adapt quickly to a new situation.

It might turn out the house, neighbors, neighborhood or city aren’t what you expected. People split up all the time, and move on average every seven years because of changing stages of life. Besides, you get lots of protections as a renter.

Rent a house to live in, and start filling your assets column as soon as possible, or you will always be working for money to pay your liabilities.